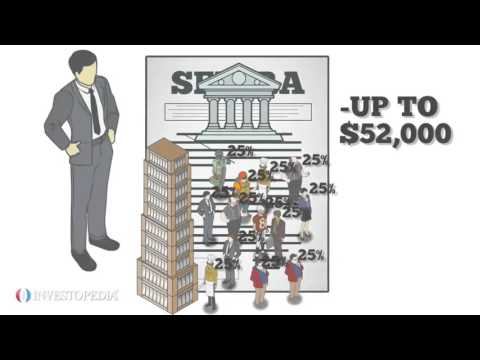

Recent studies show that most self-employed Americans are saving little, if anything, for retirement. Excuses include a lack of steady income, paying off major debt, healthcare expenses, education expenses, and business expenses. However, when the future depends on making an investment in yourself, it is worth it. The retirement saving options most preferred by self-employed workers are solo 401ks and simple IRAs. The solo or individual 401k is similar to a traditional 401k but is designed for sole business proprietors with no employees other than a spouse who works for the business. It allows for contributions both as an employee and as an employer, which means higher contribution limits compared to many other savings plans. In 2014, the employer could save up to $17,500 or $23,000 if the individual was over 50 years old, plus an additional 25% of net income up to a maximum of $52,000 or $57,500 if over 50. A simplified employee pension (SEP) IRA is suitable for individuals and businesses with employees. A SEP IRA can be opened at just about any bank or brokerage, and the business owner can contribute up to 25% of each employee's income, up to $52,000. When making a contribution, the owner must contribute for every employee, as employees do not make contributions themselves. This retirement plan is most popular with one-person businesses. Another option is the savings incentive match plan for employees (SIMPLE) IRA, which is similar to SEP IRAs but allows employees to make contributions. The employer must contribute dollar for dollar, up to 3% of each eligible employee's contribution, and 2% for those who do not contribute. In 2014, the contribution limits were $12,000, or $14,500 if over 50, and the matching requirement makes SIMPLE IRAs best for those with no employees and incomes of less than $45,000.

Award-winning PDF software

What is the difference between sep 5305 and 5305a Form: What You Should Know

Individual Retirement Accounts (IRAs) and a plan administrator (“the Plan Administrator”) providing a plan for the benefit of employees. IRA for Small Business. A plan is exempt if not subject to the IRC Section 401(a). This means that a small business that elects the IRA may be exempt from taxation on all or part of its plan's employees' compensation, whether vested or invested. Qualified small business. For purposes of IRC Section 401(a), a qualified small employer is an employer other than: (0) a labor organization that has been taxed as an exclusive employee benefit plan. Labor organization. A defined contribution plan that provides vested retirement benefits to its employees. Income tax. Any amount not includible in gross income under IRC Section 401(a) paid by or on behalf of the Plan Sponsor. Qualified Plan Sponsor. An entity that is a qualified plan sponsor under IRC Section 401(k), IRC Section 403(b), or IRC Section 457. Qualified Plan Sponsor and Plan Contribution Agreement — Vanguard The Plan Sponsor is a person, organization, or other entity with which the employee has an agreement that (i) provides for qualified pension plans for the benefit of the employees and (ii) provides for payments of qualified plan expenses (defined benefit obligations that are allowable in payment of a qualified plan benefit obligation (QBO)) to the employees. Plan Sponsor. An individual or a partnership that (i) has a plan that is exempt from the IRC Section 401(a) or the IRC Section 457(d) (the plan is “qualified”) as a labor organization, (ii) meets the requirement of IRC Section 401(a)(3) or IRC Section 457(d)(3) to be considered a qualified organization, and (iii) is a qualified Plan Sponsor for purposes of the IRC Section 401(a)(7) or IRC Section 457(d)(7). Qualified Plan Sponsor. A person, not a corporation, a partnership, a trust, or any other entity that is qualified to elect to be a Plan Sponsor under IRC Section 401(k), IRC section 403(b), or IRC Section 457(d). Qualified Plan Sponsor and Plan Document Definition.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 5305-a-SEP, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 5305-a-SEP online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 5305-a-SEP by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 5305-a-SEP from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.

Video instructions and help with filling out and completing What is the difference between sep 5305 and 5305a